ESG and Credit Risk: Past, Present and Future

-

David Harper

David has had an extensive career in investment and commercial banking credit. His experience of running the credit function at Nomura in London has given him knowledge of and insight into a wide range of transaction types, traded instruments and credit issues and allows him to deliver courses with practical and engaging examples.

This article examines why Environmental, Social and Governance (ESG) issues have come to the fore in the financial services industry, how we are beginning to think about and analyse these factors in credit risk scenarios, and what the outlook is for ESG in the near and medium term.

For the purposes of evaluating ESG factors, The European Banking Authority (EBA) recently introduced a useful definition, that is “Environmental, social or governance matters that may have a positive or negative impact on the financial performance or solvency of an entity, sovereign or individual.”

The Rise of ESG

In recent times, ESG seems to have taken on a life of its own. However, credit professionals have always known that these aspects of risk form part of any good credit analysis, and we’ve looked at them many times before. For example, the environmental liabilities that might accrue to any polluting business would be part of any credit analysis. As would the risk associated with the lien over an asset that may require potentially expensive environmental reparation in the event of a foreclosure with the bank, for example, becoming owners of the asset.

The quality of management and governance have long formed part of any assessment of credit risk. Some social factors might have been included, but with rather less emphasis in the past than on environment and governance factors. So, what exactly has changed to bring ESG so much to the fore, and for these factors to become particularly important right now?

ESG Factors in the Spotlight

It appears that there are a number of key drivers placing an increased focus on ESG. Firstly, society as a whole has become increasingly aware of, and interested in, these aspects of economic activity. Secondly, there is an overarching regulatory focus on ESG topics. Thirdly, there is an increasingly realization amongst the risk and investing communities that perhaps the rather narrow view that we have held of ESG risks in the past did not fully capture the risks and potential opportunities. Finally, the direct opportunities and risks that these ESG factors could have for businesses need to be more explicitly factored into a full risk assessment.

The investing community, perhaps a little ahead of the credit risk world, have for a while now, sought to incorporate a consideration of these externalized costs of a business into any investment analysis. These are the ESG costs faced by society in general rather than purely by the business itself as a result of any business activities – perhaps the most obvious ones being pollution and climate change.

Tackling Climate Change

The World Economic Forum identifies climate change as the single most important risk to the global economy. This reflects the warning from the Stern Report that the externality of climate change is one of the greatest failures of the market economy. These externalized costs are now being increasingly internalized, i.e. becoming a cost to the business through reputational damage, or for pollution that can be specifically attributed for example, through litigation, carbon pricing and more general impacts.

The on-going health and viability of a business may well be intimately bound up with its direct engagement with ESG factors and how well it manages these over the longer term. Of course, not all companies are exposed to the same risks, and so, the impact of ESG factors and the level of relevance and vulnerability to them can vary depending on the exact nature of the business activities of the firm. ESG relevance and ESG vulnerability scores, such as those developed by Fitch, can articulate the level of influence that ESG has on credit ratings based on credible downside ESG scenarios for both sectors and individual businesses within a sector.

A Brief History of Sustainability

At intergovernmental level, there have been a number of treaties and agreements to try and manage climate change. The United Nations Framework Convention on Climate Change was an early international agreement. The Kyoto Protocol and the Paris Climate Agreement are other key frameworks. The Paris Climate Agreement at COP21, building on the Kyoto agreement, was the first legally binding intergovernmental agreement on climate change, which asked all nations to reduce emissions and targeted amongst other things, a maximum level of global warming at 1.5 degrees centigrade, a commitment to falling greenhouse emissions, and to balance emissions and removal of greenhouse gases by the end of the century. Recently, we’ve had the latest edition of COP, COP26 in Glasgow, and COP27 in Egypt next year will seek to build upon the targets and commitments from COP26.

Conducting an ESG Analysis

Let’s take a closer look at the dynamics of ESG and how some of these factors may impact credit risk. Some of the key factors in the Environmental space associated with credit risk, may include climate change and water pollution. For Social, we can look at resource management and workers’ rights, including pay and conditions, and equal opportunities. In the Governance sphere, we may consider Board independence, diversity, corruption, shareholder rights and the appropriate role of the non-executives on various governance committees. An ESG analysis recognizes that a focus on economic growth alone is not enough, and that economic growth is only possible with sustainability through environmental protection and long-run social progress as a pre-requisite.

This brings us onto the idea of triple bottom line accounting, which along with the usual profit element must account for ESG factors, the planet and people. In the planet/environmental sphere, The World Economic Forum has estimated that more than half of the world’s economic output, some $44 trillion of economic value creation annually, is moderately or highly dependent on nature. Therefore, nature lost through environmental impacts represents a significant risk to corporate and financial stability. So, not only do we have to protect the planet, but also pay attention to the social dynamic.

The Bigger Picture – ESG and Credit

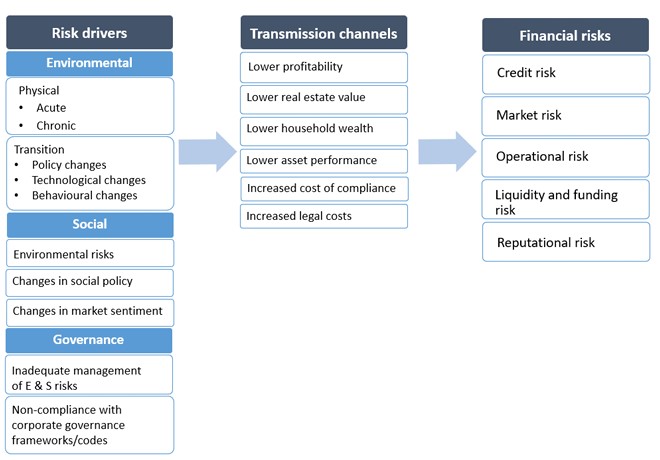

The risks and opportunities that a business faces as a result of these ESG factors is measured via transmission channels. A transmission channel is a causal chain by which ESG factors may impact an entity, business for example, or society more widely, either directly or indirectly.

The EBA has identified a set of risk drivers and the transmission channels through which they may become key financial risks, as set out in the diagram below:

These risks may not just be for specific entities but may impact the financial system as a whole with systemic consequences. These consequences may not be immediate but take time to develop. In the environmental space, for example, there are number of acute and chronic impacts for climate change. For example, a climate change driven flooding event that impacts the productive capacity for a business. Or alternatively, a ski resort that might struggle with persistently low snow fall driven by climate change, which may suppress revenue via a shorter season, or increase the costs of snowmaking, or even change the business model.

The Net Zero Horizon

The transition to low or net zero carbon economy gives rise to transition risks and opportunities. The seemingly inextricable move to electric vehicles has been a major opportunity for Tesla, but the providers of forecourts in service stations are confronted by significant capital costs installing charging points as a result. The technology that will be required in a low carbon economy is by no means certain and the risk that these changes bring with them could impact both capital expenditure and related costs. The potential for induction charging of electric vehicles, for example, may mean that plug in charging points have a limited life. The role of hydrogen vehicles, such as aircraft, and the required infrastructure is still to be determined.

Governmental policy changes are almost a constant with tax incentives and charges, together with various regulatory requirements, acting as key tools for governments in their drive to meet international climate change targets and their self-imposed climate change objectives. Compliance with regulations may give rise to risks via increased costs, taxes and transition.

A Glimpse into the Future

We have recently witnessed a number of behavioral changes to our social working habits as a direct result of the pandemic, which have affected the demand for office space and the attractiveness for city center retail, and potentially, real estate values and the opportunity for repurposing space. This shift has the potential fundamentally to alter the dynamics of the real estate market.

In the social arena, environmental risks may impact income and living costs and therefore aggregate demand. Changes in social policy may drive consumer behavior and the costs of compliance for businesses and institutions that may be affected. From a business point of view, appropriate policies in respect of diversity and discrimination may become a legal and perhaps moral obligation, and failure to meet the expected standards may give rise to reputational risks, which could be amplified through social media, and legal risks.

There is also an economic imperative for firms to embrace ESG. If an organization wishes to attract and retain the best talent, then it needs to recognize that today’s talent pool is diverse and that diversity in all its forms is a strength, from the shop floor to the boardroom.

In respect of governance, firms that fail to address the requirements of ESG management appropriately or fail to comply with the expected norms, codes or legal requirements may suffer reputational damage, sanctions or even legal actions.

Industry studies have shown that the cost of capital, both debt and equity, tends to fall as ESG scores improve. Senior leaders and managers of financial services firms may well wish to consider that improved ESG performance throughout the firm, as a result of effective credit risk management, can lead to lower business risk, decreased cost of capital and therefore enhanced value of the business.